The Best Medicare Supplement Insurance Plans in 2025

- What is the best Supplement plan for Medicare in 2025? Depending on what type of health care costs you expect this year and the types of monthly costs you want to pay, our Medigap plans review can help you decide on the type Medigap plan that’s right for you.

With 10 standardized types of Medicare Supplement Insurance plans available in most states, it’s common for shoppers to wonder which one is the top Medicare Supplement plan.

The trouble is, everyone has their own interpretation of what constitutes the “best” plan. Is it the benefits? Cost? Something else?

One way to find the best Supplement plan for Medicare is to compare the plans available where you live. With a free online plan comparison, you can see what each plan covers and how much they cost, and all from an independent source that lets you review plans from several different insurance companies.

Medicare Supplement Carrier Comparison

| Company | Pros | Cons | Learn More |

| |

User-friendly website and a long history of stability. | Currently no mobile apps for plan members. | |

|

Partnership with CVS Health | Not available in every state. | |

| Wide plan availability across the country. | Low customer reviews on BBB. |

What is the Best Medicare Supplement Plan for 2025?

To help you find the right plan for you, we’ve compiled a list of the best Medicare Supplement Insurance plans according to various criteria to help consumers like you navigate your way through the landscape.

It’s important to remember that Medicare Supplement plans (also called Medigap) are standardized by the federal government (in all states but Massachusetts, Minnesota and Wisconsin).

This means the coverage is consistent within each plan, no matter where or by whom it is sold. In other words, Medigap Plan B sold by Company 1 in New York offers the same benefits as Medigap Plan B sold by Company 2 in California.

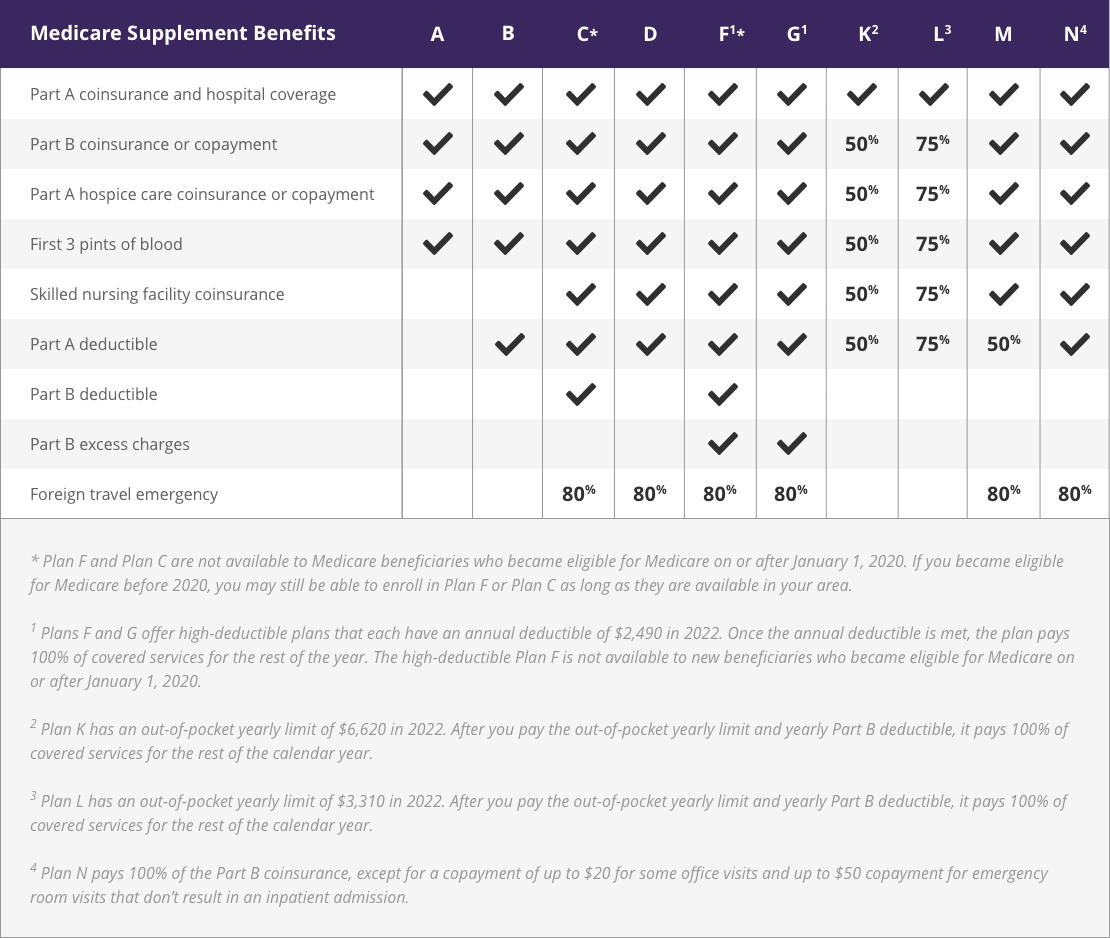

The chart below shows the 10 best Medicare Supplement plans available in most states (Massachusetts, Minnesota and Wisconsin standardize their plans differently) and a review of the combination of benefits offered by each.

| Medicare Supplement Benefits | A | B | C1 | D | F1 | G | K | L | M | N |

| Part A coinsurance and hospital costs | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Part B coinsurance or copayment | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| First 3 pints of blood | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| Part A hospice care co-insurance or co-payment | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| Co-insurance for skilled nursing facility | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ | ||

| Medicare Part A deductible | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | 50% | ✓ | |

| Medicare Part B deductible | ✓ | ✓ | ||||||||

| Medicare Part B excess charges | ✓ | ✓ | ||||||||

| Foreign travel emergency | 80% | 80% | 80% | 80% | 80% | 80% | ||||

| 1. Plans C and F are not available to new beneficiaries who became eligible for Medicare on or after January 1, 2020. 2. Plans F and G also offer a high deductible plan which has an annual deductible of $2,700 in 2023. Once the annual deductible is met, the plan pays 100% of covered services for the rest of the year. The high deductible Plan F is not available to new beneficiaries who became eligible for Medicare on or after January 1, 2020. 3. Plan K has an out-of-pocket yearly limit of $6,940 in 2023. Plan L has an out-of-pocket yearly limit of $3,470 in 2023. 4. Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to $50 for emergency room visits that don’t result in an inpatient admission. View an image version of this table. |

||||||||||

{kind=link}

Plan F: Best Medicare Supplement Plan for Coverage

As you can see by the chart above, there is one Medicare Supplement plan that stands above the rest when it comes to the benefits offered.

Plan F is the only Medigap plan to offer coverage in each of the nine benefit areas offered by this type of insurance. Members of Plan F enjoy little to no out-of-pocket expenses because their Medigap plan picks up nearly all health care costs not paid for by Original Medicare (Medicare Part A and Part B). Roughly half of all Medigap beneficiaries are enrolled in Plan F.

However, Plan F does come with one downside. Federal legislation has made Plan F off-limits to anyone who first became eligible for Medicare on or after January 1, 2020. Only those who became eligible for Medicare before that date may enroll in Plan F. Because of that rule, we can expect to see Plan F enrollment decrease every year until it eventually no longer exists.

Medigap Plan C is the only other type of Medigap plan that is subject to the same enrollment rule as Plan F. If you were eligible for Medicare before 2020, you may still be able to enroll in Plan F or Plan C if either plan is available where you live.

Plan G: Best Medicare Supplement Plan for New Enrollees

Because of the enrollment rules tied to Plan F, new enrollees are barred from enrolling in that popular plan. So what’s the best Medigap plan for someone who became eligible for Medicare after Jan. 1, 2020?

Plan G offers all of the same benefits as Plan F except that it doesn’t pay for the Medicare Part B deductible. The Part B deductible is $257 per year in 2025, so it’s a relatively small cost requirement when compared to some other types of Medicare out-of-pocket copays and deductibles. And the monthly premiums for Plan G are typically lower than those of Plan F, which can more or less cancel out the Part B deductible cost.

Plan D is another candidate for the best Medigap plan for new enrollees. Plan D offers the same coverage as Plan G with the exception of Medicare Part B excess charges. However, excess charges can usually be avoided simply by making sure to only visit health care providers who accept Medicare assignment.

Have Medicare questions?

Talk to a licensed agent today to find a Medicare Supplement plan.

Plan B: Best Medicare Supplement Plan for Basic Benefits

Some beneficiaries just want a basic Medigap plan with no thrills. Medigap Plan B checks that box, with coverage for three types of out-of-pocket Medicare costs that Medicare beneficiaries may be more likely to face that can add up quickly:

- Medicare Part A deductible

- Medicare Part A coinsurance

- Medicare Part B coinsurance

Having those three areas covered means you will likely avoid some of the biggest potential Medicare charges you could face. This can help many beneficiaries enjoy some peace of mind with a simple plan that has everything they need and nothing they don’t.

Plan N: Best Medicare Supplement Plan for Cost

Cost is always important when shopping for health insurance, and some consumers report that it is their top priority.

High-deductible Plan G and high-deductible Plan F are typically the two lowest-cost Medigap plans available. Each of these plans requires beneficiaries to meet an annual deductible before the Medigap plan coverage kicks in. In 2025, the deductible for high-deductible Plan F and high-deductible Plan G is $2,870.

This means that in exchange for a much lower monthly premium, you agree to pay up to $2,870 in 2025 for your covered services before your Medigap plan will cover most the rest of your out-of-pocket Medicare costs for the rest of the year.

Either of these plans can be a good fit for a beneficiary who doesn’t expect to use many medical services during the year and who wants to save money each month on their Medigap premiums.

Plan N is also a good plan to consider if you want a plan with lower monthly premiums. Plan N pays for most out-of-pocket Medicare costs, including 100% of your Medicare Part B coinsurance costs. The main exception is that you pay a copay of up to $20 for some of your doctor’s office visits and a copay of up to $50 if you visit the emergency room but aren’t admitted to the hospital for inpatient care.

These low – but predictable – copays allow insurance companies to typically offer Plan N at a lower monthly rate than some other Medigap plans.

Have Medicare questions?

Talk to a licensed agent today to find a Medicare Supplement plan.

Plan M and Plan N: Best Medicare Supplement Plans for Travelers

One of the health care costs that can be covered by some Medicare Supplement Insurance plans is foreign travel emergency care, or emergency care received outside of the U.S. or U.S. territories.

There are 6 Medigap plans that will pay for 80% of your foreign travel emergency care costs. Two of those plans are Plan M and Plan N, which provide coverage of foreign emergency care while typically offering lower monthly premiums than the other types of Medigap plans that also offer this coverage.

Plus, these plans also offer coverage for Medicare Part B excess charges, which allows members to see a greater variety of health care providers within the U.S. and U.S. territories.

Plan K and Plan L: Best Medicare Supplement Plans for Budgeters

Surprise or unexpected medical bills can ruin anyone’s budget. But Medicare Plan K and Plan L have annual out-of-pocket limits built into them to give beneficiaries an extra layer of protection.

For 2025, the Plan L out-of-pocket spending limit is $3,610, and the Plan K limit is $7,220. Once a plan member spends that amount on covered care, the plan then pays for 100% of all covered services and items for the remainder of the year.

Original Medicare does not include an out-of-pocket limit, which leaves beneficiaries exposed to potentially high medical bills for more serious injuries or illnesses.

How to Choose the Best Supplement Plan for Medicare

Everyone has different health care needs and spending concerns, so deciding on the best Supplement plan for Medicare for you requires assessing your own personal situation.

It can be helpful to make note of which type of care you spend the most money on to determine where your biggest savings opportunity might lie. Some questions to ask of yourself include:

- Do you travel frequently within or outside the U.S.?

- Were you eligible for Medicare before January 1, 2020 (even if you were not yet enrolled)?

- Do you have a monthly budget in mind?

- How often do you see a doctor?

Not every plan is available in every location, so the best plan for you is really the best available plan for you. There are also many other plans available, such as Medicare plan M.