High-Deductible Medicare Supplement Plan G

- Medicare Supplement High-Deductible Plan G is a type of Medigap policy. Learn how much the Medicare Plan G High-Deductible is in 2023 and find out how to compare Medicare Supplement plans to find the right plan right for you.

Many people purchase a Medicare Supplement plan – also called Medigap – to help cover their out-of-pocket Medicare costs like deductibles, copays and coinsurance.

Different types of Medicare Supplement policies may be available where you live, including High-Deductible Plan G. This plan can be cost-effective for some enrollees, but it's not suitable for everyone.

Learn how much High-Deductible Medicare Plan G costs in 2023, what this plan covers and how to request a free plan quote or speak with a licensed insurance agent to get help comparing the Medicare Supplement plans available where you live.

What Is the Medicare Plan G Plan for 2023?

High-Deductible Medicare Supplement Plan G is a type of Medicare Supplement plan. It acts as a supplement to your Original Medicare (Medicare Part A and Part B) benefits by filling some of your coverage cost gaps.

Although High Deductible Plan G typically offers relatively low monthly premiums, enrollees must pay significantly higher deductibles (including the Part B deductible) when they receive covered care than they might for most other Medigap plans.

How Much Does High Deductible Medicare Plan G Cost?

How much you pay for your Medicare Plan G with a high deductible depends on several factors, including your age and which company you buy your policy from.

Where you live can also make a significant difference to your monthly premiums.

What Is Included In Medicare Supplemental Plan G With a High Deductible?

Medicare Supplemental Plan G policies with a high deductible must provide the same benefits as regular Medicare Plan G. These include:

- Part A coinsurance

- Additional 365 days of hospital costs (beyond the Original Medicare limit)

- Part B co-insurance

- Part B copayment

- First 3 pints of blood

- Hospice copayment and co-insurance

- Nursing facility copayment and co-insurance

- Part A deductible

- Part B excess charge

- 80% foreign travel exchange

Therefore, Medicare Supplement Plan G and High-Deductible Plan G offer identical coverage. The only difference between the two plans is that regular Plan G charges higher premiums but has a lower deductible. In comparison, High-Deductible Plan G offers lower premiums with a significantly higher deductible.

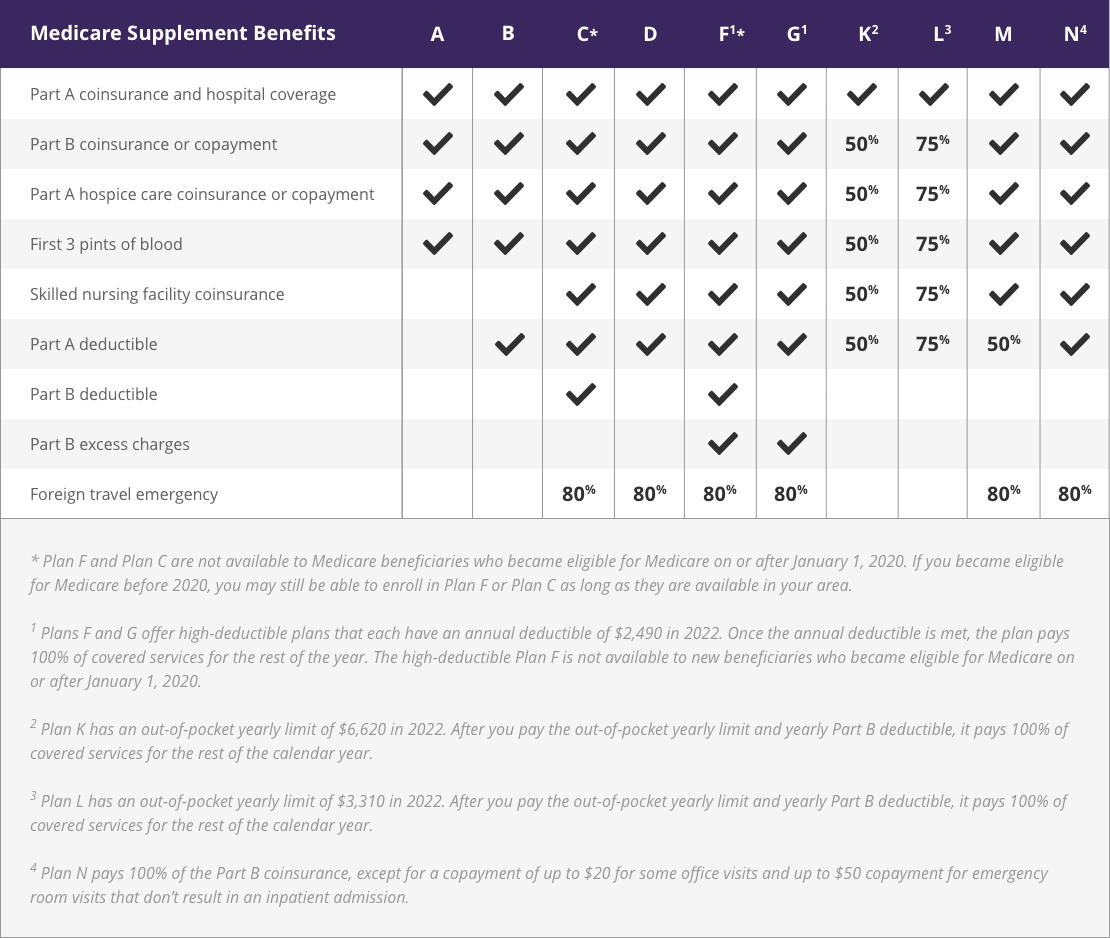

| Medicare Supplement Benefits | A | B | C1 | D | F1 | G | K | L | M | N |

| Part A coinsurance and hospital costs | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Part B coinsurance or copayment | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| First 3 pints of blood | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| Part A hospice care co-insurance or co-payment | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| Co-insurance for skilled nursing facility | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ | ||

| Medicare Part A deductible | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | 50% | ✓ | |

| Medicare Part B deductible | ✓ | ✓ | ||||||||

| Medicare Part B excess charges | ✓ | ✓ | ||||||||

| Foreign travel emergency | 80% | 80% | 80% | 80% | 80% | 80% | ||||

| 1. Plans C and F are not available to new beneficiaries who became eligible for Medicare on or after January 1, 2020. 2. Plans F and G also offer a high deductible plan which has an annual deductible of $2,700 in 2023. Once the annual deductible is met, the plan pays 100% of covered services for the rest of the year. The high deductible Plan F is not available to new beneficiaries who became eligible for Medicare on or after January 1, 2020. 3. Plan K has an out-of-pocket yearly limit of $6,940 in 2023. Plan L has an out-of-pocket yearly limit of $3,470 in 2023. 4. Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to $50 for emergency room visits that don’t result in an inpatient admission. View an image version of this table. |

||||||||||

{kind=link}

How Much Is the Medicare Deductible for Plan G in 2023?

As of 2023, the deductible for a High-Deductible Plan G policy is $2,700.

You'll need to pay the deductible when you receive care before the policy pays any benefits, which is why the monthly premiums are typically lower than for traditional Plan G or other plans. Therefore, a standard Plan G policy is worth considering if this deductible is unaffordable.

What's the Difference Between Medicare Plan G With a High Deductible and High-Deductible Plan F?

One of the key differences between Medicare Plan G with a high deductible and High-Deductible Plan F is that new enrollees can no longer purchase Plan F. Medicare beneficiaries who first became eligible after January 1, 2020, are no longer eligible for Plan F.

If you had Plan F before 2020, you can keep it. And you can apply for Plan F if you were eligible for Medicare before 2020 and Plan F is available where you live.

Otherwise, there's little to distinguish the plans from each other. However, one might be cheaper than the other in your area.

Medicare Plan F covers the Part B deductible, and Plan G doesn't.

Do Guaranteed Issue Rights Apply to High-Deductible Plan G?

You may have guaranteed issue rights to purchase Medigap policies in certain situations without medical underwriting. This means that a company must offer you a Medigap policy and cannot increase your premiums due to your health status.

There are several situations in which you may have guaranteed issue rights. For example, you might have the right to purchase a Medigap policy if you move outside your existing Medicare Advantage plan's coverage area or your insurer leaves Medicare.

You can only assert your guaranteed issue rights to buy High-Deductible Plan G if you have a qualifying life event or if you apply during your Medigap Open Enrollment Period.

Your Open Enrollment Period starts as soon as you are at least 65 years old and enrolled in Medicare Part B. This open enrollment period only lasts for six months, and it may be the only time you have guaranteed issue rights unless you later experience a qualifying life event.

Where Can I Buy Medicare Plan G With a High Deductible in 2023?

Where to purchase a High-Deductible Plan G policy depends on the carriers in your area.

It's generally a good idea to speak to a licensed insurance agent to find suitable providers where you live and for help selecting a plan that meets your needs and financial circumstances.

Is a High-Deductible Plan G Policy Right for Me?

A High-Deductible Plan G policy could be a good option if you prefer to save money on the cost of monthly premiums. However, it's essential to ensure that you are comfortable meeting the considerable deductibles if you require care. It's also worth considering this type of plan if you regularly travel overseas.