Medicare Plan F vs Plan G: Compare the Two Most Popular Medigap Plans

- Learn the differences between Medicare Plan F and Plan G, including pros and cons and how to enroll in the best Medicare Supplement (Medigap) plan for you.

As you approach retirement age, it's important to understand the differences between Medicare Plan F vs Plan G and make an informed decision on which Medigap plan is right for you. Comparing these two plans can be an arduous undertaking, as each presents its own advantages and disadvantages.

In this Medicare Supplement Insurance review, we'll discuss Medicare Supplement (also called Medigap) Plan F vs. Plan G in detail, exploring what they offer, how to compare them effectively and how to enroll in Medicare Plan F vs Plan G so that you can have financial security during your golden years.

Have Medicare questions?

Talk to a licensed agent today to find a plan that fits your needs.

Table of Contents:

- What is Medicare Supplement Plan F?

- What is Medicare Supplement Plan G?

- How to Compare Medigap Policies F and G

- Pros and Cons of Medicare Plan F vs Plan G

- How to Enroll in a Medicare Supplement Plan

- Is Medicare Part F better than Part G?

- Why should I switch Medigap Plans from plan F to plan G?

- Why is Plan F being discontinued?

- How much does Plan F cost in 2024?

- Conclusion

What is Medicare Supplement Plan F?

Medicare Supplement Plan F is a type of insurance that can pay some of the healthcare costs Medicare Part A hospital insurance and Part B medical insurance don't pay for.

Medicare Supplement plans are offered by private insurance companies, and each type of plan (designated with a letter such as Plan F) pays for a different combination of healthcare costs not covered by Original Medicare (Part A and Part B), which is administered by the federal government.

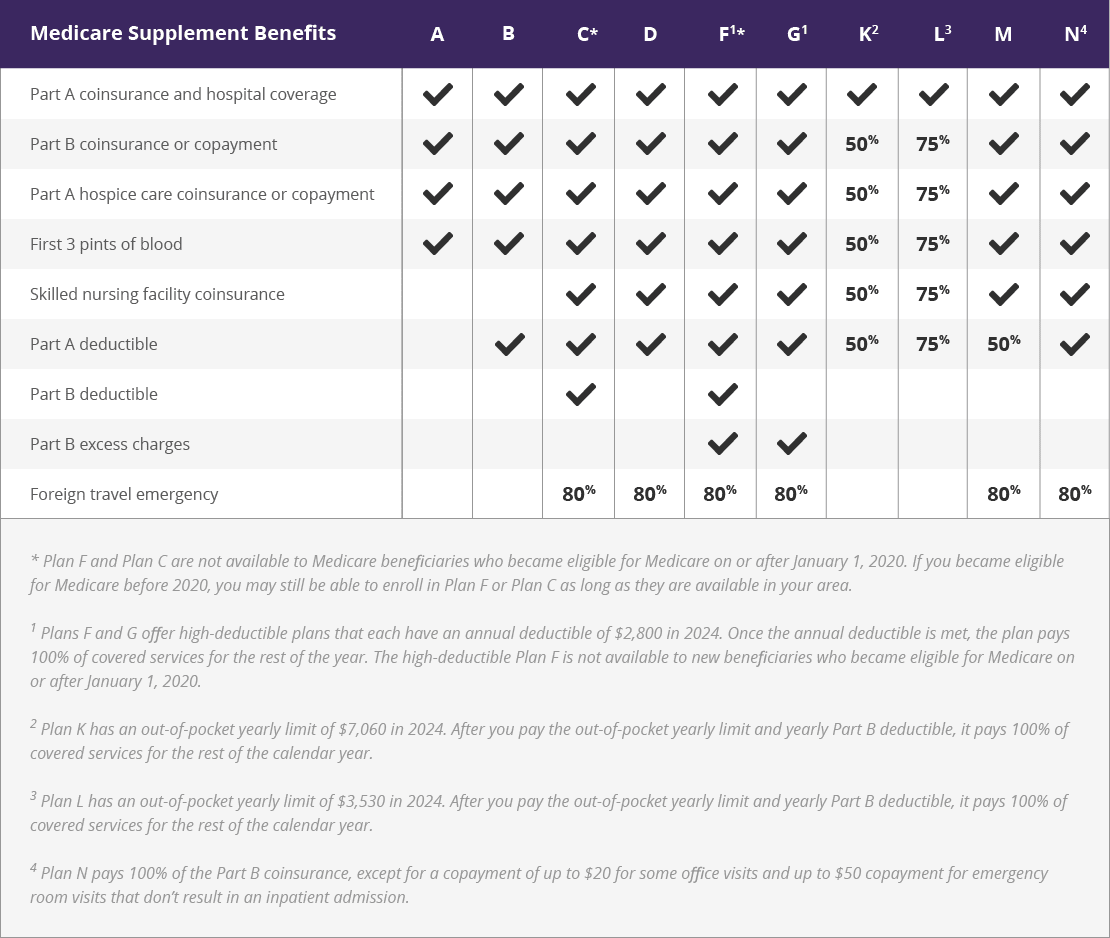

| Medicare Supplement Benefits | A | B | C1 | D | F1 | G | K | L | M | N |

| Part A coinsurance and hospital costs | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Part B coinsurance or copayment | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| First 3 pints of blood | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| Part A hospice care co-insurance or co-payment | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| Co-insurance for skilled nursing facility | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ | ||

| Medicare Part A deductible | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | 50% | ✓ | |

| Medicare Part B deductible | ✓ | ✓ | ||||||||

| Medicare Part B excess charges | ✓ | ✓ | ||||||||

| Foreign travel emergency | 80% | 80% | 80% | 80% | 80% | 80% | ||||

| 1. Plans C and F are not available to new beneficiaries who became eligible for Medicare on or after January 1, 2020. 2. Plans F and G also offer a high deductible plan which has an annual deductible of $2,870 in 2025. Once the annual deductible is met, the plan pays 100% of covered services for the rest of the year. The high deductible Plan F is not available to new beneficiaries who became eligible for Medicare on or after January 1, 2020. 3. Plan K has an out-of-pocket yearly limit of $7,220 in 2025. Plan L has an out-of-pocket yearly limit of $3,610 in 2025. 4. Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to $50 for emergency room visits that don’t result in an inpatient admission. View an image version of this table. |

||||||||||

{kind=link}

Plan F covers a number of out-of-pocket expenses associated with Medicare Parts A and B covered services, including deductibles, coinsurance, copayments and other cost sharing.

Having a Medigap plan like Plan F can be advantageous in several ways:

- You are safeguarded from any hefty medical bills such as hospital costs due to the gaps in coverage left by Original Medicare.

- Any doctor, provider, hospital or health care facility that accepts Original Medicare Part A and Part B will accept your Medicare Supplement plan.

If you often travel or live in an area with limited healthcare providers that take only Original Medicare medical insurance, then having a Medigap plan could prove beneficial since it grants access to many healthcare providers throughout state borders or even internationally depending on your provider’s network size and reach.

The cost associated with purchasing a Medigap policy varies based on factors such as age at time of purchase, location (state), gender and tobacco use status. Since premiums can vary between insurers, it is wise to shop around and compare quotes for the best price.

It's important to note Plan F is only available to beneficiaries who were first eligible for Medicare before 2020. If you became eligible for Medicare on or after January 1, 2020, you aren't eligible to sign up for Plan F. In this case, Plan G is the most comprehensive Medigap plan you may consider.

Key Takeaway: Medigap Plan F provides comprehensive coverage for out-of-pocket expenses associated with Parts A and B of Original Medicare, but Plan F is only available to beneficiaries who were eligible for Medicare before 2020.

Have Medicare questions?

Talk to a licensed agent today to find a plan that fits your needs.

What is Medicare Supplement Plan G?

Plan G is the most popular Medicare Supplement plan for new Medicare beneficiaries.1 In fact, this plan covers some of the same costs not covered by Original Medicare that Plan F pays for, with one exception: it does not cover the annual Medicare Part B deductible. You will be required to pay the Part B deductible annually out of your own pocket prior to receiving coverage. In 2025, the Part B deductible is $257 for the year.

The benefits provided by Plan G are similar to those provided by other plans like Plan F and N, including coverage for hospital costs, medical services, preventive care, emergency care and more. The key difference between these plans is that Plan G does not cover the Part B deductible while Plans F does.

Premiums for this plan may differ based on geographic location and the insurance companies that offer plans where you live. Generally speaking, Plan G premiums tend to be lower than those associated with other plans like Plans F.

Overall, Medicare Supplement Plan G can provide peace of mind knowing that many expenses related to healthcare are taken care of without having to worry about large out-of-pocket costs associated with Original Medicare alone.

Key Takeaway: Plan G is a great option for those looking to save on Medicare Supplement premiums without sacrificing coverage, as it provides similar benefits as Plans F and Plan N but does not cover the Part B deductible. That said, one must remember to factor this cost into their budgeting decisions before committing to Plan G.

Similarities and Differences Between Medicare Plan F vs Plan G

Plan F and Plan G are two of the most popular Medicare Supplement plans available to those who are eligible for Medicare.1 Both plans provide cost coverage benefits beyond what Original Medicare offers, but it is important to weigh the distinctions between them when deciding which one is right for you.

Medicare Plan F and Plan G each cover a number of the gaps in Original Medicare, including:

- Part A deductible

- Part A coinsurance

- Part B coinsurance or copayment

- First three pints of blood used in a transfusion

- Skilled nursing facility (SNF) coinsurance or copayment costs

- Hospice care coinsurance or copayment costs

- Medicare excess charges (up to 15% more than the Medicare-approved amount for a covered service)

In addition to these benefits, both plans also cover emergency medical services while traveling outside of the United States.

The major difference between these two plans is that Plan F covers the annual Medicare Part B deductible while Plan G does not. Even with the increasing cost of Original Medicare Part B deductible over time, it may make sense financially to opt for Plan G since it usually has a lower monthly premium than Plan F.

Another key difference between Plan F and Plan G is while they offer similar coverage, Plan G is the most comprehensive Medigap plan for new Medicare beneficiaries.

Due to recent legislation from the federal government, Plan F and Medicare Supplement Plan C are no longer available to new beneficiaries. If you were eligible for Medicare before 2020, you can still apply for Plan F if it's available where you live. If you have Plan F before 2020, you can keep it.

Have Medicare questions?

Talk to a licensed agent today to find a plan that fits your needs.

Pros and Cons of Medicare Supplement Plans F and G

The pros of Medicare Supplement Insurance Plan F vs Plan G include:

- Plan F is the most comprehensive Medigap plan, as the plan pays 100% of more of Medicare-approved costs than any other Medigap plan. It also offers a high-deductible option which allows you to pay lower premiums while still having coverage for all approved expenses after meeting your deductible.

- Plan G covers nearly the same list of approved Medicare health insurance expenses as Plan F except for the Medicare Part B annual deductible. Before receiving coverage from insurance, you will have to cover any costs related to Part B out-of-pocket. Nevertheless, the cost of premiums may be lower than Plan F depending on your location and desired coverage. Plan G also offers a high-deductible version that typically offers even lower monthly premiums.

The cons of Plan F vs Plan G include:

- The biggest downside with both Medicare plans is that they do not provide prescription drug coverage.

Original Medicare beneficiaries can add a Medicare Part D prescription drug plan – which only covers prescription drugs – or enroll in a Medicare Advantage plan (also called Medicare Part C) that covers their Original Medicare health benefits and may typically provide prescription drug coverage. - If you choose the high-deductible version of either plan, you may face increased costs since more money is needed up front before any coverage kicks in.

How to Enroll in a Medicare Supplement Plan

To be eligible for a Medicare Supplement plan, you must be enrolled in both Part A and Part B Medicare benefits. Some states may require additional qualifications such as age or disability status.

Once eligibility has been confirmed, the next step is to contact a licensed insurance agent to compare the plans that are available specifically in your ZIP code. You can also request a free plan quote online. Once you find the plan you want and confirm your eligibility, the licensed agent can help you enroll.

Your new Medigap plan coverage should typically begin within one month after submission, provided no further documentation is needed from you by the insurer prior to approval and activation of your policy.

Medicare Plan F vs Plan G FAQs

Is Medicare Part F Better Than Part G?

Medicare Plan F provides slightly more comprehensive coverage than Plan G. However, it also has higher premiums and deductibles than Part G does. Ultimately, the best choice will depend on your specific needs and financial situation. Those considering either plan should speak with a Medicare agent to determine which one is right for them.

Why Should I Switch From Plan F to Plan G?

Switching from Plan F to Plan G can be a beneficial move. By switching to Plan G, you may save money on premiums since it is usually less expensive than Plan F.

Ultimately, it comes down to what you require and your financial situation. Though you can switch plans at any time, switching when you don't have guaranteed issue rights allows insurance companies to user medical underwriting to determine your premiums and potentially deny you coverage.

Why Is Plan F Being Discontinued?

The Medicare Access and CHIP Reauthorization Act of 2015 (MACRA) prohibits Plan F or Plan C from being sold to new Medicare beneficiaries. The MACRA was enacted to encourage beneficiaries to select more economical treatment options. As a result, Plan F is longer an option for new enrollees as of January 1, 2020.

How Much Do Medigap Plans Cost in 2025?

In 2024, the average annual premium for Plan F was around $200 per month. The average Plan G annual premium was roughly $140 per month, which shows some beneficiaries may be able to save money if they switch plans.2

It's important to keep in mind that the best time to switch Medigap plans is when you have guaranteed issue rights which protect you from medical underwriting.

The cost of Plan F or Plan G in 2024 will be determined by a variety of factors, including your age, where you live and potentially your health. Generally speaking, premiums for Medicare Supplement Plans may be based on an enrollee’s age when they first enroll in the plan; as such, rates may vary from year to year.

To determine your exact rate for Medicare Plan F vs Plan G in 2025, you should contact a licensed insurance agent or request a free plan quote online.

Have Medicare questions?

Talk to a licensed agent today to find a plan that fits your needs.

Conclusion

Medicare Supplement Plans F and G both offer valuable benefits to those eligible for Medicare. Though Plan F pays for more Medicare-covered costs, it may not be the most cost-effective choice when compared to Plan G.

It is important to consider your individual needs before making a decision on which plan best fits you, as well as compare different providers' rates for each Medicare Plan F vs Plan G option. Ultimately, selecting either of these plans can help guarantee that you receive quality medical care at a cost-effective rate.

Discover the benefits of Medicare Plan F vs Plan G to ensure you have good health and financial security as you age. Make an informed decision today by comparing coverage options, costs and eligibility requirements.

AHIP. (Feb. 2023). The State of Medicare Supplement Coverage: Trends in Enrollment and Demographics. https://www.ahip.org/documents/202301-AHIP_MedicareSuppCvg-v03.pdf.

Internal sales data provided by TZ Insurance Solutions LLC, 2023. This data is based on the Medicare Supplement Insurance policies TZ Insurance Solutions LLC has sold. It is not a comprehensive national average of all available Medicare Supplement Insurance plan premiums.