Medicare Supplement Plans Comparison Chart 2024

- This chart comparing Medicare Supplement (Medigap) plans outlines the benefits of each of the 10 different standardized Insurance plans available in most states. Compare plans to learn what’s covered.

Medicare Supplement Insurance, also called Medigap, are private insurance plans that pay for some of the out-of-pocket Medicare costs that you typically face when you have Original Medicare (Medicare Part A and Part B).

But what are those covered expenses, and how does one Medigap plan compare to another?

The Medigap chart below offers a comparison of the benefits covered by each type of standardized Medicare Supplement Insurance plan that’s offered in most states. In this chart comparing Medicare Supplement plans, you’ll find a summary of each benefit along with some important need-to-know information about how to compare between plans.

Have Medicare questions?

Talk to a licensed agent today to find a plan that fits your needs.

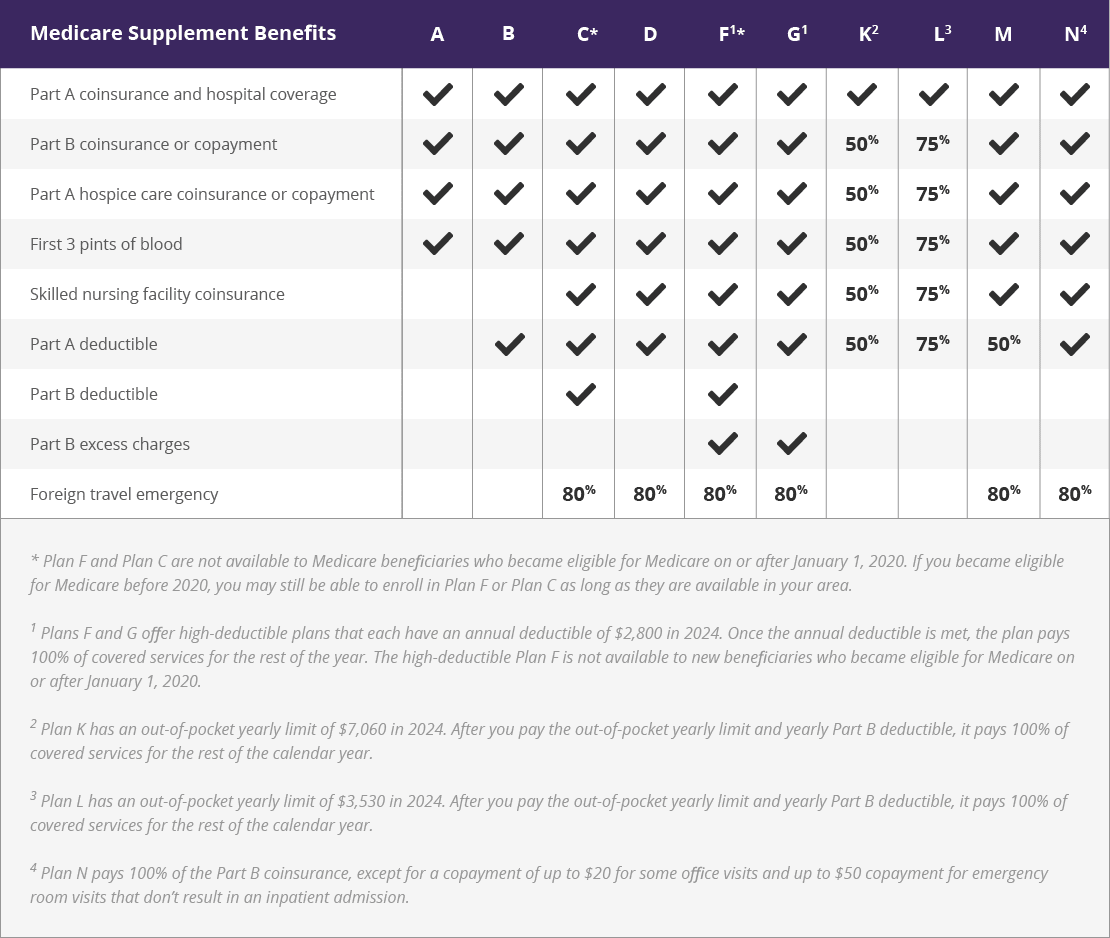

| Medicare Supplement Benefits | A | B | C1 | D | F1 | G | K | L | M | N |

| Part A coinsurance and hospital costs | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Part B coinsurance or copayment | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| First 3 pints of blood | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| Part A hospice care co-insurance or co-payment | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| Co-insurance for skilled nursing facility | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ | ||

| Medicare Part A deductible | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | 50% | ✓ | |

| Medicare Part B deductible | ✓ | ✓ | ||||||||

| Medicare Part B excess charges | ✓ | ✓ | ||||||||

| Foreign travel emergency | 80% | 80% | 80% | 80% | 80% | 80% | ||||

| 1. Plans C and F are not available to new beneficiaries who became eligible for Medicare on or after January 1, 2020. 2. Plans F and G also offer a high deductible plan which has an annual deductible of $2,800 in 2024. Once the annual deductible is met, the plan pays 100% of covered services for the rest of the year. The high deductible Plan F is not available to new beneficiaries who became eligible for Medicare on or after January 1, 2020. 3. Plan K has an out-of-pocket yearly limit of $7,060 in 2024. Plan L has an out-of-pocket yearly limit of $3,530 in 2024. 4. Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to $50 for emergency room visits that don’t result in an inpatient admission. View an image version of this table. |

||||||||||

{kind=link}

What Are the Differences in Medicare Supplement Plans?

Each type of Medigap plan offers a different combination of Medicare cost coverage benefits. Some plans cover certain out-of-pocket Medicare expenses in full, while other plans may only partially cover the same costs, if at all.

As you analyze the chart comparing Medicare Supplement plans, you should consider which of the following Medicare costs you want to have covered by your plan in exchange for paying your monthly Medigap plan premium. Keep in mind that some plans that cover more benefits may have higher monthly premiums.

Part A Deductible

Part A requires you to pay a deductible of $1,632 per benefit period in 2024 before your Part A coverage kicks in. A benefit period begins the day you are admitted to a facility as an inpatient and ends once you have not been an inpatient for 60 consecutive days.

Because the Part A deductible isn’t an annual deductible, it’s important to note that you could potentially have to pay the deductible more than once in a year if you experience multiple benefit periods in that year.

Each type of Medigap plan except for Medigap Plan A cover all or a percentage of your Part A deductible, even if you have multiple benefit periods in one year.

Part A Hospital Coinsurance

If you have an inpatient hospital stay that lasts longer than 60 consecutive days in a benefit period, you’re required to pay a Medicare Part A coinsurance cost of $408 per day in 2024. This coinsurance goes towards what Medicare Part A covers for things like your hospital room, your food, your hospital bed and other inpatient costs.

If you stay in the hospital longer than 90 days, your daily coinsurance increases to $816 for each “lifetime reserve day,” for which you only have 60 to use over the course of your lifetime. After your lifetime reserve days are all used up, you’re responsible for the full cost of your inpatient expenses.

Each type of Medicare Supplement plan covers the Part A coinsurance in full.

Part B Deductible

Part B requires you to pay an annual deductible of $240 pear year in 2024 before your Part B coverage kicks in. Medicare Part B covers some services – such as your annual flu shot – in full without forcing you to first meet your Part B deductible. For most covered services, however, your deductible applies.

Only two Medicare Supplement plans – Plan F and Plan C – cover the Part B deductible.

It’s important to note that while Plan F is the most popular Medicare Supplement plan, Plan F and Plan C are both no longer available for new Medicare beneficiaries who became eligible for Medicare on or after January 1, 2020. We’ll explain more about that below.

Part B Coinsurance

Medicare Part B pays for things like covered visits to your doctor’s office, the costs for durable medical equipment such as wheelchairs and other outpatient health care costs.

Part B typically requires you to pay a coinsurance of 20% of the Medicare-approved amount for any covered services or devices after you meet your annual Part B deductible.

20% coinsurance costs may not amount to high amounts when applied to something like a wheelchair. Some costs, such as outpatient cancer treatment, can come with potentially high Part B coinsurance costs, however.

Each type of Medicare Supplement plan covers all or a percentage of your Part B coinsurance costs.

First Three Pints of Blood

If you need a blood transfusion while you’re in the hospital, Medicare coverage for blood only kicks in beginning with the fourth pint of blood that you need.

The hospital may be able to give you donated blood from a blood bank, if they have it. In that case, the first three pints of blood would likely be free of charge. In some cases, however, the hospital may have to buy blood. In this case, they would charge you the costs for the first three pints of blood.

Each type of Medigap plan covers all or a percentage of the cost of the first three pints of blood.

Part A Hospice Care Coinsurance and Copayments

Medicare hospice coverage requires coinsurance payments of 5% for inpatient respite care and copays of no more than $5 for prescription drugs and other products designed for pain relief and symptom control.

Each type of Medicare Supplement plan covers all or a percentage of your Medicare Part A hospice coinsurance or copay costs.

Skilled Nursing Facility Care Coinsurance

If you’re admitted for an inpatient stay at a skilled nursing facility (SNF) that lasts longer than 20 days, Medicare Part A requires a daily coinsurance payment of $204 per day in 2024. After 100 days, you’re responsible for all of your inpatient costs.

Eight out of the ten standardized Medicare Supplement plans cover all or a percentage of your skilled nursing facility coinsurance costs.

Part B Excess Charges

Most doctors and providers accept Medicare assignment, which means they accept the Medicare-approved amount for a service and will only charge you that amount.

If a doctor or provider doesn’t accept Medicare assignment, they are allowed to charge you up to 15% more than the Medicare-approved amount for their services or products, in what is known as an “excess charge.”

Medigap Plan F and Plan G are the only two types of Medicare Supplement plans that cover Part B excess charges.

Foreign Travel Emergency Care

Only under rare circumstances does Medicare Part A or Part B provide any coverage for emergency medical care outside of the U.S. and U.S. territories.

Several, but not all, types of Medicare Supplement plans cover 80% of your foreign travel emergency care costs after you meet an annual deductible.

Out-of-Pocket Limit

Two types of Medicare Supplement plans offer an annual out-of-pocket spending limit. Once you reach that spending limit on out-of-pocket costs for covered care, the plan covers 100% of the amount of covered services and items for the remainder of the year.

Plan K and Plan L are the only two types of Medicare Supplement plans that include an out-of-pocket spending limit. For Plan K, the spending limit is $7,060 for the year in 2024, while the 2024 spending limit for Plan L is $3,530.

Learn More About Medicare

Join our email series to receive your free Medicare guide and the latest information about Medicare and Medicare Supplement Insurance (Medigap).

By clicking "Sign me up!" you are agreeing to receive emails from HelpAdvisor.com

Thanks for signing up!

Your free Medicare guide is on the way.

Make sure to check your spam folder if you don't see it.

How to Compare Medicare Supplement Plans

When comparing Medicare Supplement plans, it helps to consider what plans are available, how much they cost, when you can enroll and what plans you may be eligible for.

1. Find Out Which Plans Are Available Where You Live

Medicare Supplement Insurance plans can be used all over the country when you visit any doctor, hospital or provider who accepts Medicare. But specific Medicare Supplement plans can only be purchased in the area in which you live.

Not every county or zip code will have the same selection of different types of plans, so be sure to find out which Medicare Supplement plans are available in your area.

2. Compare Prices

The offered by the Medicare Supplement Insurance plans in the comparison chart above are standardized and remain consistent no matter where the plan was purchased. Plan G in California covers the same costs as Plan G in Maine. But one thing that does fluctuate is the pricing of monthly plan premiums.

To use the example above, Plan G in California may offer the same benefits as Plan G in Maine, but Plan G premiums may be more expensive in California. There also might be two different insurance companies in your area that both offer the same plan but at different prices.

3. Know When You Can Apply

The first month that you are 65 years old and enrolled in Medicare Part B marks the first month of what’s called your Medigap Open Enrollment Period. This period lasts for six months and is the best time to apply for a Medicare Supplement plan.

During your six-month Medigap Open Enrollment Period, you can apply for a Medicare Supplement Insurance plan with a guaranteed issue right, which means insurance companies cannot use medical underwriting to determine your plan premiums or eligibility.

There may be other situations that qualify you for guaranteed issue rights, such as losing your Medigap plan through no fault of your own because the company stopped offering that plan. You might also qualify for guaranteed issue rights if you move to an area where your current Medicare Supplement plan is no longer offered.

If you apply for a Medigap plan during a time when you don’t have a guaranteed issue right, a Medicare Supplement Insurance company is allowed to use medical underwriting in your application process, which means they could potentially charge you more for the plan or deny you coverage altogether based on factors such as your health.

4. Explore Your Options if You Are Under 65

Federal law does not require insurance companies to sell Medigap policies to beneficiaries who are under 65 and have qualified for Medicare because of a disability. There are 33 states, however, that require insurance companies that sell Medigap plans to make at least one plan available to people under 65.

If you have Medicare under age 65, be sure to find out if Medicare Supplement plans are available to you in your state.

5. Confirm whether you are eligible for Plan F or Plan C

Only people who were eligible for Medicare before January 1, 2020 are eligible to enroll in Medigap Plan C or Plan F. If you did not become eligible for Medicare until that date or later, you will not be allowed to enroll in either of these plans.

What Is the Best Medicare Supplement Plan for 2024?

When choosing a Medicare Supplement Insurance plan, consider how you anticipate using your Medicare coverage. For example, if you have a medical condition like diabetes that requires frequent utilization of Medicare Part B for diabetes treatment supplies, you may want to enroll in a Medigap plan that provides 100% coverage of Part B coinsurance costs.

If you do a lot of traveling and could potentially see a variety of different providers, it may be wise to enroll in a plan that offers full coverage of Part B excess charges, in case you’re forced to see a provider who doesn’t accept Medicare assignment.

You can look at the Medigap chart above or take advantage of an independent licensed insurance agent to get help comparing, choosing and enrolling in a Medicare Supplement plan. An agent can typically tell you which plans are available in your area, help you compare costs and benefits, answer your questions and guide you through the application process.

Have Medicare questions?

Talk to a licensed agent today to find a plan that fits your needs.